A Nigerian borrower has triggered fresh debate over digital lending practices after publicly accusing PalmPay of using aggressive recovery methods, including allegedly reaching out to people in his contact list just days after his loan became overdue.

A Nigerian borrower has triggered fresh debate over digital lending practices after publicly accusing PalmPay of using aggressive recovery methods, including allegedly reaching out to people in his contact list just days after his loan became overdue.

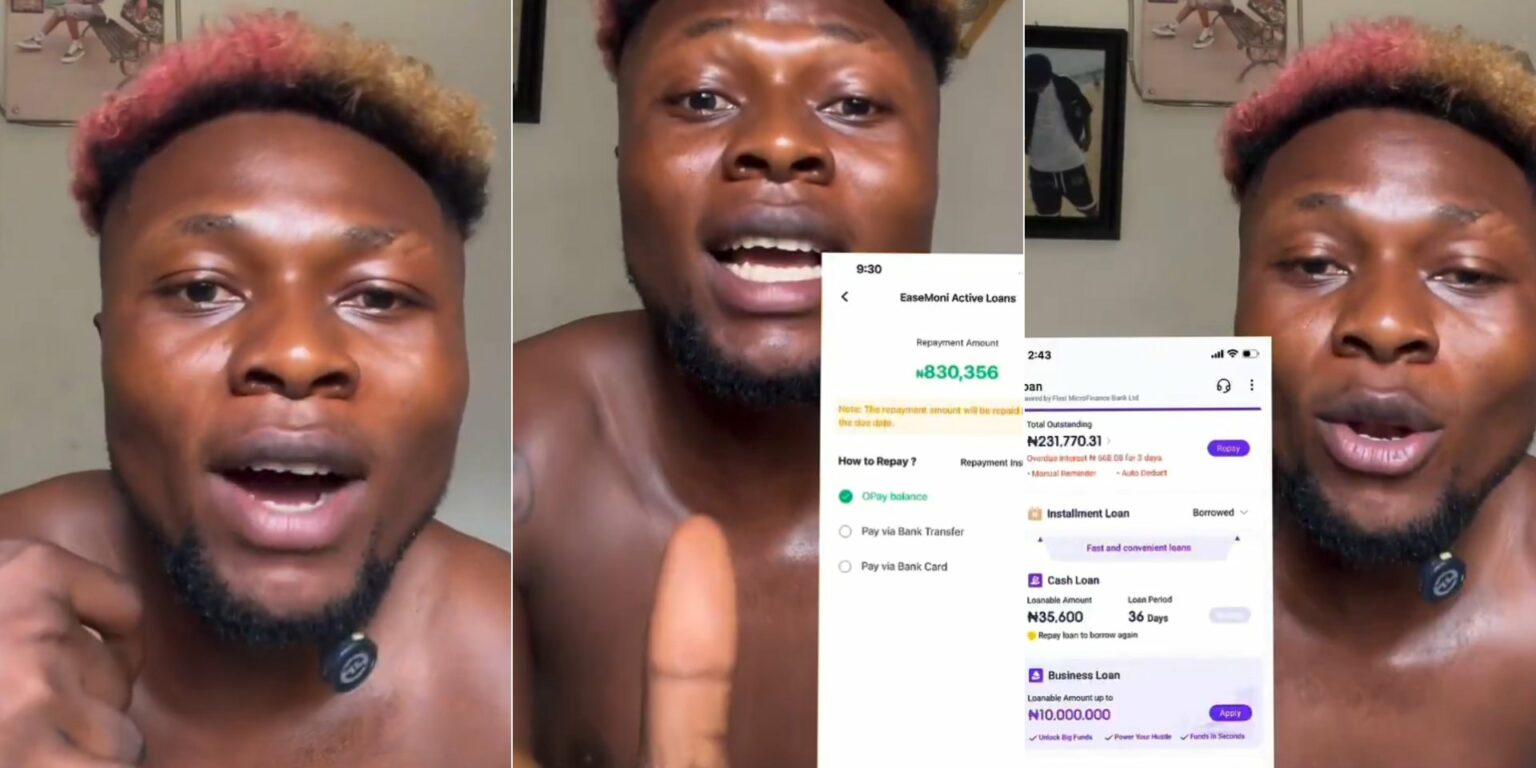

In a viral social media outburst, the man contrasted his experience with OPay, claiming he owes OPay ₦800,000 but has only received direct reminder calls about repayment. By contrast, he alleged that PalmPay escalated recovery efforts within three days of his missed payment by sending messages to individuals in his phone contacts — a tactic that has long drawn criticism in Nigeria’s fast-growing digital lending market.

His comments, laced with anger and frustration, reflected a broader public concern: how far lenders should be allowed to go in pursuing debt without crossing into harassment, intimidation, or violations of customer privacy.

Renewed scrutiny on digital loan recovery methods

Digital lending has expanded rapidly in Nigeria over the last five years, driven by smartphone adoption, tighter household finances, and easy access to instant credit through mobile apps. Platforms such as PalmPay and OPay have become widely used for payments, transfers, and increasingly, consumer lending.

But alongside that growth has been a steady stream of complaints over debt collection practices.

Borrowers have repeatedly accused some lenders of sending threatening messages, contacting relatives and colleagues, or broadcasting debt notices to third parties listed in their phones. Privacy advocates argue that such tactics can amount to digital shaming — weaponising embarrassment as a collection strategy.

Regulators have stepped in before.

The Federal Competition and Consumer Protection Commission has in recent years investigated several digital lenders over alleged privacy breaches, harassment, and unethical loan recovery practices. Some apps were sanctioned or removed from app stores following complaints tied to unauthorised access to borrowers’ contact lists and abusive collection methods.

What is alleged — and what is not confirmed

At present, the borrower’s allegations against PalmPay remain a personal account shared online and have not been independently verified. PalmPay has not publicly responded to the specific accusation contained in the viral post.

It is also unclear whether messages were directly sent to contacts, what the content of those communications may have been, or whether consent terms in the platform’s user agreement cover such access in any form.

Those details matter because under Nigeria’s evolving data protection framework, companies handling customer data are expected to operate within clear consent, lawful processing, and privacy safeguards.

Why this matters beyond one borrower

For ordinary Nigerians, the controversy speaks to a larger tension in the digital credit economy: quick loans often come with collection systems many users do not fully understand until repayment problems begin.

With inflation squeezing incomes and more households relying on short-term borrowing to bridge expenses, defaults are becoming more common. That raises the stakes around how fintech lenders balance debt recovery with customer rights.

Aggressive tactics may recover some loans, but they can also damage brand trust, invite regulatory scrutiny, and deepen public suspicion of digital lending products.

PalmPay’s next move will likely shape the conversation. If the company addresses the allegation directly, it could clarify whether the incident reflects company policy, third-party recovery agents, or an isolated complaint.

Until then, the backlash is another reminder that in Nigeria’s booming fintech sector, speed and convenience are only part of the story — accountability is increasingly becoming the real test.